Defaults in an opaque corner of China’s local debt market have surged to a record high, ensnaring investors who’d assumed the securities had an implicit guarantee from the state.

It wasn’t supposed to be this way. Last year, confronted with a wave of bad debt issued by municipalities’ financing arms, the country’s central government took action. It gave local governments permission to raise around 2.2 trillion yuan ($309 billion) in new bonds to help repay creditors and ordered state banks to provide additional refinancing support.

Those measures drove borrowing costs to a record low and investors rushed back into the market, clamoring to buy bonds and loans. But one segment didn’t get fixed. Failures of so-called non-standard products, which are fixed-income investments that aren’t publicly traded, surged to record levels. While there is no official tally of the size of the sector, analysts estimate it to be around $800 billion.

Stock Market Today: All You Need To Know Going Into Trade On Oct. 25

The defaults have proved costly for many retail investors.

Take Lulu Fang. The 60-year-old owner of a small trading company said she lost her life savings of 15 million yuan when she bought so-called trust products tied to Guizhou province in the southwest of the country. She was counting on a stable return of about 8%, much higher than what she would earn from depositing the funds in a bank. Instead her investment was wiped out when the products defaulted last year.

Faced with possible foreclosure on her apartment in Shenzhen due to her failure to make mortgage payments, she joined more than 100 other investors on multiple trips to the trusts and government offices to plead for repayment.

“My life is a total mess now,” she said. “I have worked my entire life and put all the money I saved for retirement into the products. I was told these were safe. That was a lie.”

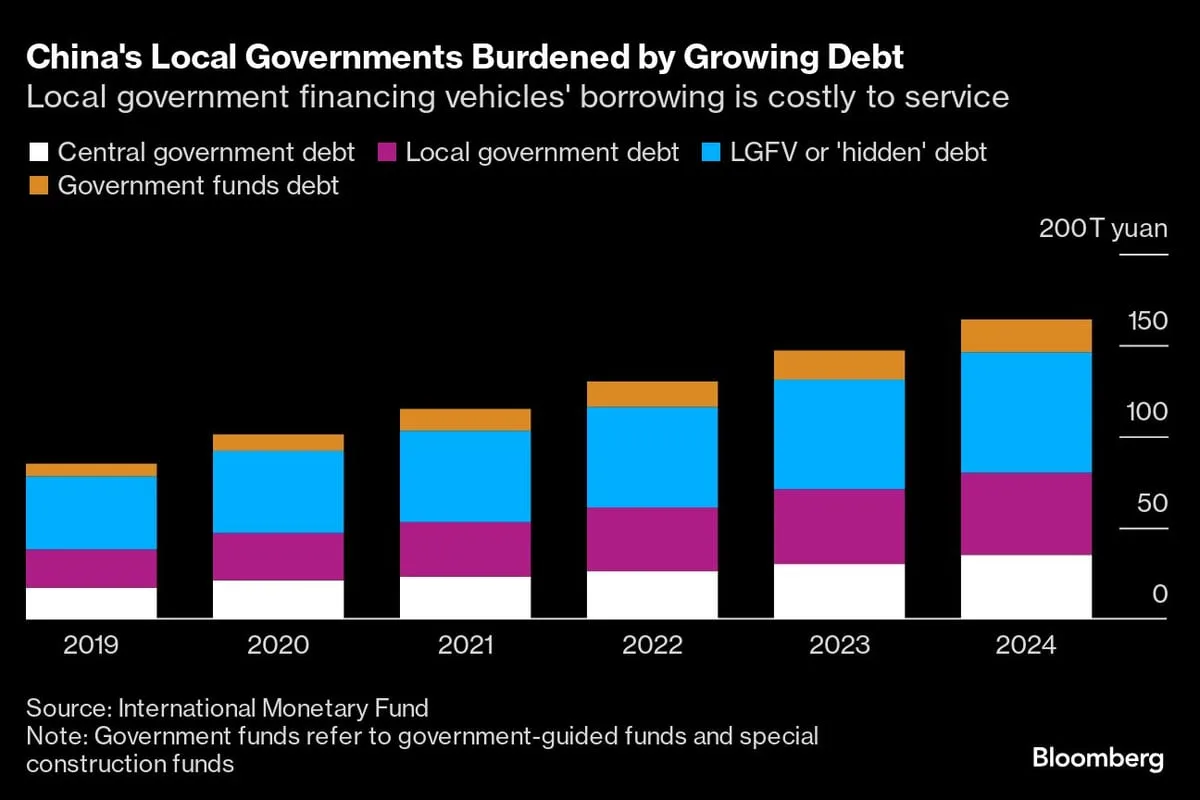

The country’s towns, cities and provinces have used so-called local government financing vehicles (LGFVs) to fund infrastructure projects, including road and ports. However, projects financed by the LGFVs don’t necessarily earn money. That makes them dependent upon support from the government.

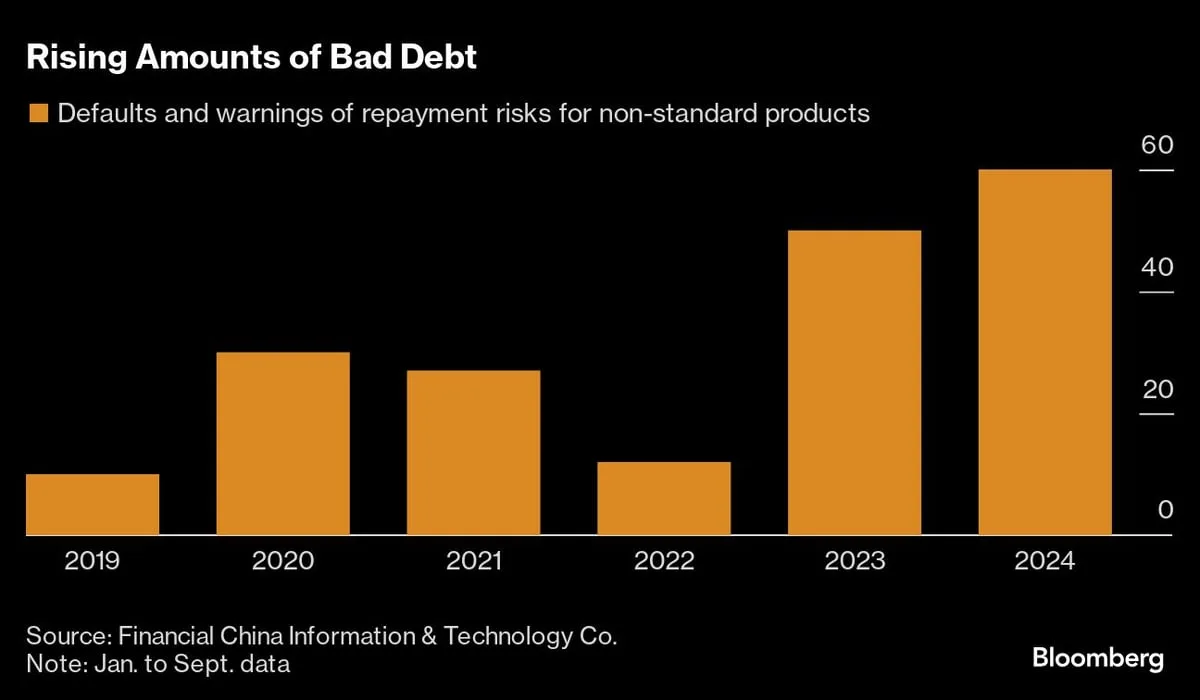

In the first nine months of this year, 60 non-standard products tied to LGFVs have defaulted or warned of repayment risks, up 20% from the same period last year, according to data compiled by Financial China Information & Technology Co. The figure was the highest since at least 2019, the data showed.

The issuers of the debt generally do not disclose the total amount. Of the 60 cases tallied by FCI&T this year, 40 did not give any figures. The remaining 20 products that defaulted or warned of repayment risk totaled about 4.55 billion yuan.

This stands in stark contrast to publicly traded bonds issued by LGFVs. Local governments have prioritized these securities, which are favored by institutional investors and there has never been a default. Since non-standard products are typically sold to investors in private placements, local authorities have less incentive to help them.

Rise With Profit: Petroleum Board Proposes Removal Of Exclusivity, ITC Q2 Results, US Stocks Gain

“Although China has introduced a series of policies to address LGFV debts, the policies need to ensure the repayment of LGFVs’ public bonds as they are part of the capital market,” said Laura Li, a managing director at S&P Global Ratings. “Should they default, it will endanger financial stability and social stability.”

There is some hope for investors who own the defaulted debt. The central government is considering allowing local authorities to issue as much as 6 trillion yuan in bonds through 2027 to refinance off-balance-sheet debt, according to people familiar with the matter. If this happens, it opens the possibility for LGFVs to broaden their support for non-standard products. Still, that is not a given and some analysts doubt that would happen.

“If the new round of vows to cut hidden debt actually come true, local authorities will still prioritize LGFV bonds over non-standard debt when any products need support,” said Wang Chen, co-founder of Belt & Road Origin (Beijing) Tech Co., a provider of credit-risk analysis. “The new plan’s impact on the non-standard market would depend on the actual scale of policy support, and how such resources could be allocated among different regions and entities.”

Many of the defaults have occurred in the trust industry. Trust fund products are usually unlisted and sold via channels such as banks and securities firms to companies, financial institutions and high net worth individuals with a minimum investment threshold of 1 million yuan. They usually offer regular fixed payments annually or semi-annually with a set period of six months to five years.

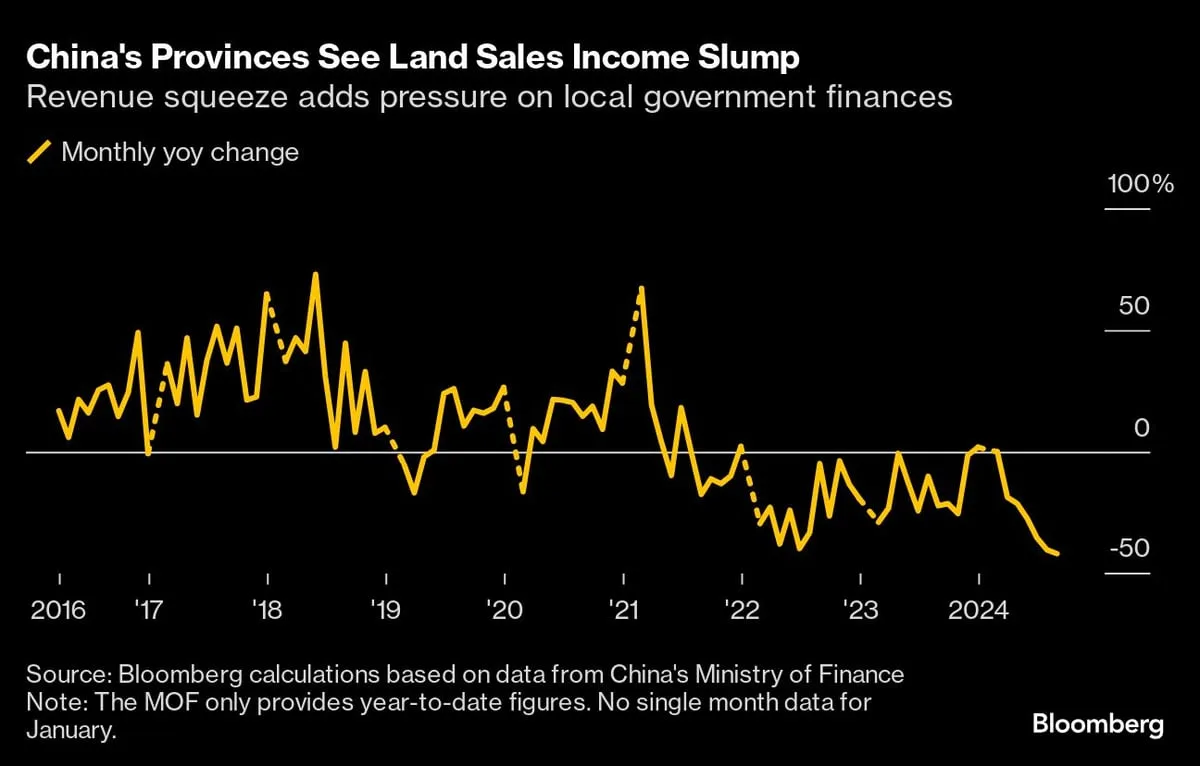

The LGFVs have turned to the non-standard products because local governments are increasingly cash-strapped due to the country’s economic slow-down and a sharp decline in land sales. Regulators have tightened restrictions on the sale of bonds by LGFVs, forcing them to seek alternatives. They typically pay 7-8% interest on non-standard products compared with 3% interest for listed bonds.

“LGFVs definitely have the need to finance via non-standard channels, despite the high costs,” said S&P’s Li. “But their policy priority is low, so the default rate remains at a high level.”

Asian Stocks Mixed After Wall Street Posts First Gain This Week

Those defaults have left retail investors like Fang desperate for assistance, but the experience of a fellow retail investor suggests she doesn’t have much chance of getting her money back.

Jason Lai’s investment of three million yuan into an LGFV-guaranteed wealth management product went sour five years ago. Lai, an employee at a Beijing-based state-owned enterprise, has traveled four times to the regional city of Anshun, seeking repayment.

“Since 2019 when the product first defaulted, I could only manage to reclaim about 10% of the principal,” said Lai. “I won’t buy any of such products in the future.”

. Read more on Global Economics by NDTV Profit.